The integration-platform-as-a-service market has bifurcated into: vendors with a broad go-to-market strategy that tackle a wide range of enterprise integration scenarios; vendors that focus on the more specific use cases. This Magic Quadrant focuses on the first category, enterprise iPaaS.

Strategic Planning Assumption

By 2021, enterprise iPaaS will be the largest market segment in application integration middleware, potentially consuming the traditional software delivery model along the way.

Market Definition/Description

An integration platform as a service (iPaaS) solution provides capabilities to enable subscribers (aka “tenants”) to implement data, application, API and process integration projects involving any combination of cloud-resident and on-premises endpoints. This is achieved by developing, deploying, executing, managing and monitoring integration processes/flows that connect multiple endpoints so that they can work together.

iPaaS capabilities must include:

- Communication protocol connectors such as FTP, HTTP, Advanced Message Queueing Protocol (AMQP), Applicability Statement 1 (AS1)/2/3/4, and others

- Application connectors/adapters for SaaS and on-premises packaged applications

- Data formats such as XML, JavaScript Object Notation (JSON), Abstract Syntax Notation One (ASN.1) and others

- Data standards such as Electronic Data Interchange for Administration, Commerce and Transportation (EDIFACT), Health Level Seven (HL7), SWIFT and others

- Data mapping and transformation

- Data quality

- Routing and orchestration

- Integration flow development and life cycle management tools

- Integration flow operational monitoring and management

iPaaS capabilities can also include:

- Full life cycle API management

- B2B ecosystem management

- Internet of Things (IoT) integration

An iPaaS solution is typically used for cloud service integration (CSI), application-to-application integration (A2A), business-to-business integration (B2B) scenarios and, increasingly, for mobile application integration (MAI) and IoT integration scenarios.

Gartner considers an iPaaS solution to be enterprise iPaaS (EiPaaS) if it:

- Is designed to support enterprise-class integration projects; that is, projects requiring, high availability/disaster recovery (HA/DR), security, service-level agreements (SLAs) and technical support from the provider

- Provides appropriate user experiences to the end user of the platform to allow the subscriber to develop integration capabilities independent of the EiPaaS provider’s professional services

- Can be used for multiple integration scenarios including application integration and data integration use cases

- Is marketed for a broad range of use cases, verticals and industries

- Is fully managed by the vendor for patching and upgrades; client-managed software components are not considered to be part of an EiPaaS offering

- Provides flexibility for the deployment of the runtime engine for a number of hybrid deployment options

This market only includes companies that provide public EiPaaS offerings to be used by the subscriber for the purpose of integrating applications, data sources and APIs. Vendors that sell just iPaaS-enabling software, provide iPaaS capability only embedded in other xPaaS solutions, such as application PaaS (aPaaS), or iPaaS capabilities only embedded within SaaS applications, are not considered to be an EiPaaS vendor.

Magic Quadrant

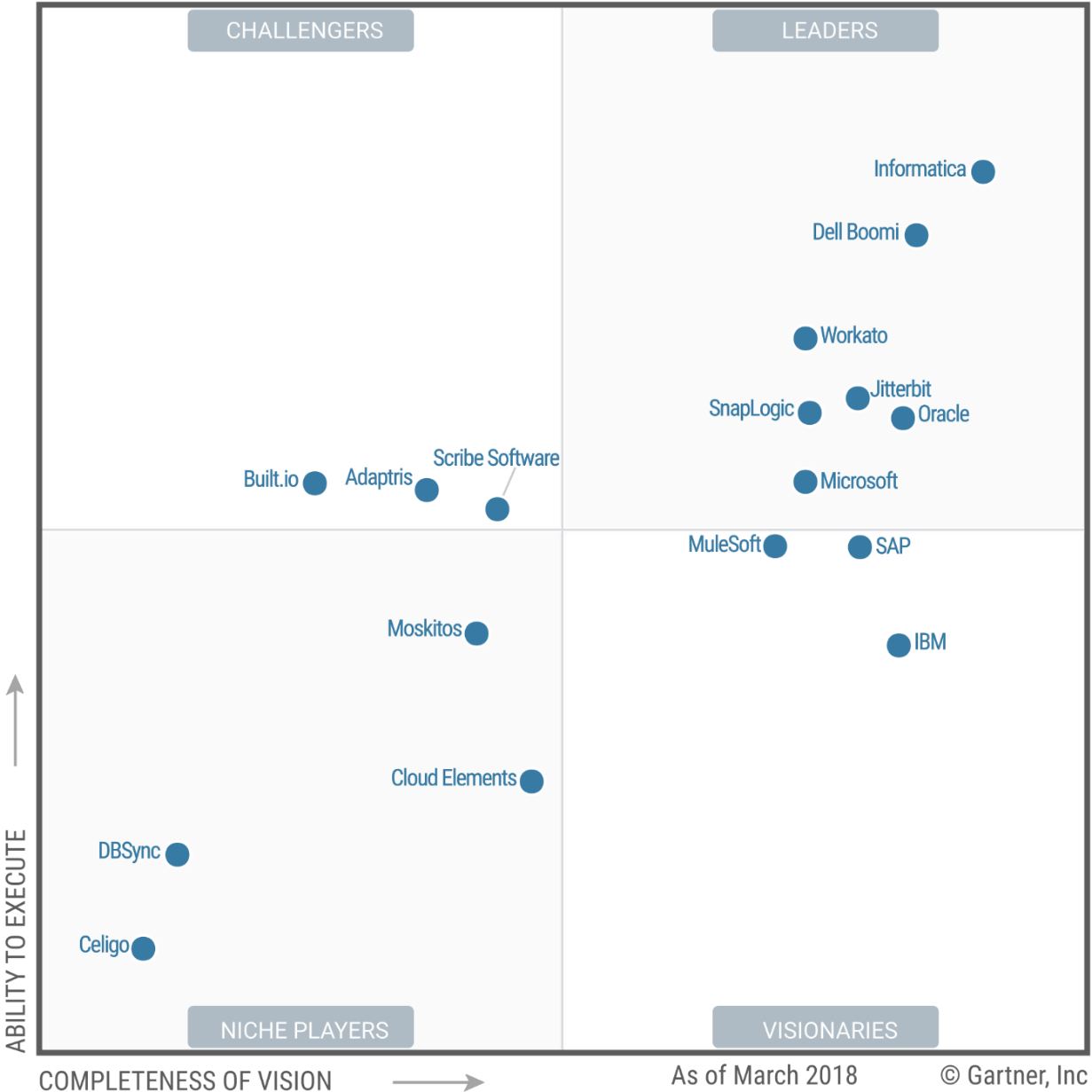

Figure 1. Magic Quadrant for Enterprise Integration Platform as a Service

Source: Gartner (April 2018)

Vendor Strengths and Cautions

Adaptris

Established in 1998 in London, U.K. and acquired by RELX Group in 2015, independently operated Adaptris provides an EiPaaS offering, Cirrus, for use in B2B, cloud-based and on-premises application integration. The vendor’s strong electronic data interchange (EDI) heritage has helped it expand into the B2B-focused EiPaaS market for clients seeking software, services and/or managed service offerings.

Adaptris also offers integration brokerage — an outsourcing offering to support document exchange between trading partners. While Cirrus is available as a stand-alone offering, the vendor often sells it and the integration brokerage service together — with a primary focus on IoT and big data support as a solution set in the agricultural-food industry.

Strengths

- Targeted industry traction: With a focus on selling EiPaaS and integration brokerage together, along with APIs for the IoT and strong support for B2B integration, Adaptris has an established recognition for supporting agriculture-related solutions. This industry-oriented strategy is expanding its reach into ecosystem markets, including the animal health, financial and travel industries.

- Capitalizing on data ecosystem: Providing EiPaaS capability alongside big data offerings to link, cleanse, structure and deliver data using machine learning techniques, extends Adaptris’ platform versatility, in addition to its B2B integration strength, in order to broaden opportunities for data and analytics scenarios.

- Customer satisfaction keeps pace with growth: Adaptris’ partnering posture toward companies results in a positive customer experience, encompassing the presale process, the selling process and the postsale relationship. Having an installed base of more than 5,400 EiPaaS customers, Adaptris added about 970 customers in 2017, including global enterprises adopting Cirrus for their cloud and on-premises integration needs.

Cautions

- Mind share: Adaptris has limited visibility and market share in the EiPaaS market, due to a lack of visibility outside its customer base of the agri-food industry as well as a comparatively rare presence in competitive situations.

- Guidance and support for evolving solutions: As usage and requirements become increasingly complex, reference customers desire guidance and support to broaden EiPaaS use cases and implement evolving solutions and upgrade paths from Adaptris’ offerings.

- Evolution of new market offerings and global strategy: As the focus continues to shift toward big data and analytics, and opportunities through its ownership by RELX, Adaptris’ plans and its platform — which is undergoing transformation — remain largely unknown to buyers in this market.

Built.io

Built.io is based in San Francisco, California, U.S., and expanded into a PaaS solution business in 2013. It offers EiPaaS, mobile back-end cloud services and content management cloud services (cmsPaaS), which are three distinct offerings and can connect with each other. The vendor’s EiPaaS offering, Built.io Flow, focuses on quick and easy enablement of integration flows. It connects mobile apps, cloud services (such as Salesforce, G Suite, Amazon Web Services [AWS] and others), social networking (such as Slack) and devices/things (such as connected cars) via prebuilt integration templates and model-driven design.

Built.io Flow has three editions: Express for business users, Enterprise for IT teams, and Flow Embed for OEM partnerships. Built.io Flow is available in the cloud as PaaS. It also supports a hybrid deployment model with an Enterprise Gateway to connect applications on-premises (such as Oracle and SAP), as well as on serverless and container architectures through the Built.io serverless deployment (for AWS Lambda and Kubernetes, for example).

Strengths

- Client growth: Built.io added more than 2,500 paying customers and more than 7,000 free-trial users during 2017, and its year-over-year revenue growth was well above the market average, albeit from a small revenue base. The vast majority of this customer growth was driven through smaller deals; the revenue growth through several significant enterprise deployments. Built.io is investing in its channel and partner network to support the new Built.io Flow Embed offering.

- Customer experience and satisfaction: Reference customers scored Built.io highly in overall customer satisfaction and experience, value for money, evaluation and contracting, delivery and execution, and services. This performance, coupled with a broad multipersona and high-productivity approach, helped Built.io drive the second highest number of projects per customer in this Magic Quadrant.

- IoT and mobile focus: Built.io supports hybrid deployments and a variety of use cases, including for IoT and mobile, along with SaaS integration. By connecting Built.io Flow and its mobile back-end cloud service offering, Built.io Backend, customers can create and integrate microservices used in mobile applications and IoT deployments.

Cautions

- Limited versatility: Although Built.io added several API management capabilities in 2017, its features here are relatively new, and less comprehensive and mature than those of some competing EiPaaS offerings. It provides minimal or missing support for EDI-based B2B integration, ground-to-ground integration (due to the lack of an on-premises EiPaaS deployment option), industry-specific standards — such as Health Insurance Portability and Accountability Act (HIPAA), Health Level-7 (HL7), Association for Cooperative Operations Research and Development (ACORD) and others — and big data/analytics use cases. Large organizations seeking a more versatile and functionally rich platform may find limited appeal in Built.io Flow.

- Geographic strategy: Built.io is less visible than some EiPaaS competitors, particularly outside North America where it has limited commercial and support operations. This may limit its ability to serve customers operating internationally. It has modest plans to invest in marketing and its partner network, in order to increase market awareness and traction in select countries across EMEA and Asia/Pacific during 2018.

- Ecosystem community features and policy management: Built.io’s roadmap includes plans and investment to add a B2B partner portal for partner self-service integration, and to offer policy management and enforcement capabilities. However, Built.io Flow currently lacks these features.

Celigo

Celigo entered the EiPaaS platform market in August 2008, when it released a cloudstream to integrate Salesforce to NetSuite. In March 2016, Celigo launched Integrator.io, its second-generation EiPaaS offering, which replaced its original Celigo Integrator offering. Built on top of its EiPaaS offering, Celigo provides a wide range of prepackaged integrations (for example, Celigo SmartConnectors) and packaged composite applications (such as Celigo Productivity Apps), which are sold as independent SaaS offerings.

Strengths

- Small or midsize business (SMB)-focused strategy: Celigo is laser-focused on supporting the fast-growing SMB market in which the company aspires to a dominant role, especially in the NetSuite and Salesforce ecosystems. These ambitions are supported by simple user experiences targeting “ad hoc” and “citizen” integrators.

- Diversified go-to-market strategy: In addition to a classic IT-centric EiPaaS proposition, Celigo’s go-to-market strategy strongly targets business buyers. The rich and advanced set of SmartConnectors is designed to appeal to business users. The Celigo Productivity Apps, sold by a dedicated sales organization, are totally focused on business buyers.

- Adoption: Celigo was able to add approximately 300 new clients during the past 12 months, growing its total client base by 30% to more than 1,300. Given the limited market presence, as reflected in the Gartner EiPaaS client survey, this was a respectable growth and almost on a par with the market average.

Cautions

- Versatility and functional coverage: Integrator.io lacks API management capabilities and provides minimal support for EDI-based B2B, mobile app, IoT and big data/analytics integration. Moreover, the offering received below-average scores from its reference clients for functional completeness. These limitations will be only partially addressed by the roadmap for the next 12 months, which implies that Celigo might not attract organizations looking for a highly versatile and functionally rich EiPaaS offering.

- Geographic presence: Celigo currently has data centers and offices in the U.S. only. During 2018, there are plans to open offices in Europe and Asia/Pacific to better serve its small (12%) but growing international market.

- Customer satisfaction: Celigo was evaluated by its reference customers as being among the lowest with regard to overall experience with the vendor and value for money. However, no score was below a 4, out of 5, which highlights the very competitive nature of the enterprise EiPaaS market.

- Developer experience: Celigo’s reference clients evaluated it as among the lowest with regard to all three integration developer experiences — specialist, ad hoc and citizen — despite the company’s focus on ease of use.

Cloud Elements

Founded in 2012 and based in Denver, Colorado, U.S., Cloud Elements provides an API-centric integration platform that focuses on solving the problem of organizing existing APIs for easy consumption.

Cloud Elements’ approach is to provide normalized access to applications and data sources. Cloud Elements enables a canonical data model approach and sets of uniform (canonical) RESTful APIs. Categories of services (that is, CRM or cloud storage) or collections of normalized resources (such as Invoice, Product or Employee) are made available as API Hubs. Each API Hub is mapped into multiple corresponding SaaS applications (for example, Salesforce and SugarCRM for the CRM Hub) via customizable prepackaged connectors (or “Elements”). The Cloud Elements platform is used to create and extend Elements, as well as to create integration flows that can also be exposed as APIs. A separate interface, Elements Connect, provides a simplified means of selecting and deploying the prepackaged integration flows.

Strengths

- Innovation: Cloud Elements’ approach to integration through the creation of normalized APIs, very rich connectors and unified data models is differentiating. Among EiPaaS vendors, it has a strong API management capability. The Cloud Elements model is particularly well-suited to organizations that have either many SaaS products in the same domain (that is, HCM or finance) or a fluid environment where they desire to easily swap in/out similar products. It is also well-suited to organizations that are leaning toward rationalizing and governing their data models.

- Indirect channel/sales strategy: Cloud Elements’ go-to-market model has a focus on OEMs/independent software vendors (ISVs). Cloud Elements services are provided as white-labeled, easy-to-deploy integration services to the customers of SaaS application providers. The end-user organizations that end up leveraging Cloud Elements as a result of this model, may find it appealing to extend its usage to additional use cases.

- Breadth of connector types: Cloud Elements has a catalog of 150 prebuilt “Elements” across 17 API Hubs (categories of products). Customers and system integrators (SIs) can develop and publish additional custom Elements and Hubs.

Cautions

- Platform versatility: Cloud Elements’ approach includes EiPaaS, API management and iSaaS. However, the EiPaaS solution lacks some capabilities of a fully featured tool, such as EDI-style B2B integration, managed file transfer (MFT) and workflows (involving tasks performed by humans). Reference customers for Cloud Elements indicated that their purchase was associated with an API initiative rather than a cloud ERP or CRM project, as is more typical of EiPaaS customers.

- Complex value proposition for enterprise IT: The Cloud Elements focus on attracting ISVs has resulted in complex messaging that is well-tuned to developers, but almost inaccessible to enterprise IT leaders.

- Market presence: While Cloud Elements has data centers in North America and EMEA, its current customers are 90% in North America and 10% in EMEA. Future plans include opening an EMEA headquarters early in 2018. Until then, Cloud Elements will have limited appeal for EMEA-centric organizations.

- Customer experience: There was an insufficient number of responses from Cloud Elements’ reference customers to draw any meaningful conclusions from the survey results. However, they did provide comments about issues around the quality of documentation, as well as a concern around the ability of the platform to scale. Prospective clients should question Cloud Elements about these issues.

DBSync

Founded in 2009, and based in Brentwood, Tennessee, U.S., DBSync provides capabilities for integrating data among databases, applications and cloud sources, via on-premises and cloud deployment models.

With a focus on the integration needs of SMBs to support CRM and accounting operations, DBSync’s EiPaaS offering, Cloud Workflow, provides replication and integration capabilities for provisioning, monitoring and managing data across heterogeneous applications, and data and cloud environments. Environments include Salesforce, Microsoft Dynamics, Sage Intacct, SkuVault, NetSuite and QuickBooks. DBSync pursues a direct-sale strategy and is increasing its focus on providing integration capability via a partner network. ISVs and solution providers can extend their platforms to offer Cloud Workflow functionality on their environment for their customer base.

Strengths

- Strength and stability of functionality: DBSync offers strong data and application integration functionality applied to heterogeneous data and application types, with a historical strength in addressing SMBs. DBSync’s experience in integrating data, process of accounting, and e-commerce-related cloud applications are regarded as key points of value in its adoption.

- Expanding market reach: DBSync has added channel focus by enhancing its partner portal, developer community, ISV and co-sell arrangements, and continues to expand its market reach. DBSync has a focus on portability and service enablement of Cloud Workflow integration artifacts. It aims to simplify integration through its ApiCode functionality (for images rendered in Docker, AWS and Microsoft Azure, for example) and service wrapper based on the Swagger API framework.

- Customer focus: DBSync’s partnering posture toward companies — understanding their business needs and appropriately delivering solutions — results in strong customer relationships and a positive perception of value relative to cost.

Cautions

- Coverage and market resonance: Organizations seeking providers for an enterprisewide range of EiPaaS scenarios find DBSync’s position in the market to be relatively narrow. Buyers attracted to DBSync’s solution are primarily SMB customers addressing targeted or departmental-level integration projects.

- Technical help and professional services: Implementations reflect concerns with the ease of navigating technical help for troubleshooting and best practices. Customers desire improvements in self-help support and availability of professional services to guide usage, administration and additional capabilities.

- Hybrid deployments: Although users of DBSync increasingly have a mix of cloud and on-premises runtime deployment models, reference customers cite the need for easier implementation to enable hybrid integration platform (HIP) scenarios.

Dell Boomi

Dell Boomi, based in Chesterbrook, Pennsylvania, U.S., is a business unit within Dell Technologies. It provides EiPaaS capabilities for application and data integration as part of its AtomSphere unified PaaS platform. AtomSphere also provides API design and management, master data hub, B2B management, workflow automation and app development.

AtomSphere is available in several editions, differentiated by target market, use case, breadth of functionality and number of connected endpoints. It also targets the B2B integration market via a dedicated AtomSphere edition and an associated managed service. Functional add-ons and further connections are also available. All editions include standard support with premium options.

Strengths

- Sales execution: Adding more than 1,500 clients in 2017, Dell Boomi’s total installed base now amounts to more than 7,000 global, large or midsize organizations worldwide. At the same time, revenue grew more than 50%, to about $150 million, positioning the company among the largest iPaaS providers. This was achieved while keeping overall customer satisfaction above average and improving its value-for-money scores from reference customers.

- Product functionality and versatility: AtomSphere is a well-proven, powerful and versatile platform that its reference customers use to support complex cloud-to-cloud-to-on-premises, mobile app, B2B and IoT integration requirements, as well as API publishing. The MDM, API management, EDI managed service and managed multicloud runtime deployment offerings (on AWS and Microsoft Azure), along with the new workflow automation tool, help diversify Dell Boomi’s proposition and increase its cross-selling opportunities.

- Vertical/industry strategy: Dell Boomi is closely aligned with major horizontal technology partners such as Salesforce, Workday and NetSuite, and has alliances with global SIs such as Accenture and Deloitte. Unlike many EiPaaS providers, the company also targets multiple industry verticals via specific sales and marketing plans and solution templates. It also addresses the healthcare sector, in partnership with Dell Technologies.

- Offering strategy: Dell Boomi has restructured its development organization and plans to increase R&D investment by 50% to support an ambitious 12-month roadmap. This includes improved API management, IoT, event processing, workflow automation and widespread use of artificial intelligence (AI)/machine learning (ML) to improve the multipersona user experience, optimize operations and deliver deeper technical and business insights.

Cautions

- Ease of development and citizen integrator support: Reference customers scored AtomSphere as below average in user experience. Historically, ease of development has been a strength for Dell Boomi. These ratings indicate that it failed to keep pace with other players’ innovations in this area.

- Pricing: Although reference customers gave Dell Boomi above-average scores for professionalism in the sale process, they also score the company’s flexibility and adaptability in final negotiations as below average.

- Multicloud and citizen integrator support: Although Dell Boomi plans to make AtomSphere available on AWS, some leading competitors have more aggressive plans for multicloud support. Despite the planned investment in AI/ML, Dell Boomi’s vision for citizen integrator support is behind that of its leading competitors.

- Geographic strategy: Despite sales and marketing investments in EMEA and Asia/Pacific, about 75% of AtomSphere clients are in North America, affecting the allocation of its sales and support personnel. Prospects planning international/global EiPaaS deployments may find Dell Boomi less appealing than competitors with a broader geographic presence.

IBM

Founded in 1911, and based in Armonk, New York, U.S., IBM has an EiPaaS offering called Application Integration Suite on Cloud. The suite includes three components, which can also be purchased individually. These are: IBM App Connect Professional, focused on ad hoc and citizen integrators; IBM Integration Bus on Cloud, focused on integration specialists; and IBM API Connect, which provides capabilities to manage and secure integration flows when exposed as APIs.

Strengths

- Vision and product evolution: IBM’s HIP-aligned strategy for its EiPaaS solution, as part of a broader IBM Cloud Integration Platform vision, continued to make good progress through 2017. A balanced focus for addressing a broad set of personas and use cases, ever-increasing platform unification and extensions, and a comprehensive roadmap that includes leverage of cognitive features through Watson, is building on IBM’s strength and reputation in integration.

- Packaging model: IBM’s packaging strategy is flexible, aggressive and modeled on demand trends. By adopting a hybrid-oriented approach to packaging — including free trial option and new “Flex Bundle” — customers can choose between any pricing model (capital expenditure or operating expenditure) and deployment style (on-premises, cloud, hybrid) across a broad range of use cases. As customers can also purchase specific capabilities and functionality at different levels, this high degree of flexibility enables both existing clients and newcomers to start small and expand use cases over time.

- Global staff/skills presence: IBM benefits from having an established global presence in hardware and software, its services network and a large partner network. With more than 3,000 partners, it has the network and reach to influence both the size and shape of the global EiPaaS market.

Cautions

- Customer experience and satisfaction: Reference customers scored IBM’s EiPaaS offering as below average in customer satisfaction and experience. This performance was consistent across all vendor and product-support-related categories for IBM, including value for money, delivery and execution, and the sales and negotiation process. Despite articulating a strong vision that is underpinned by compelling technology, IBM is working to resolve challenges in delivering a high-quality engagement experience from its field and delivery organizations. This may pose commercial and implementation challenges for clients in the interim period.

- Market traction: Although IBM’s EiPaaS revenue grew above the market average in 2017, Gartner estimates its direct-paying customer base grew less than the market average. IBM’s combined direct and indirect customer count is, therefore, still relatively small when compared with the market leaders. This suggests that IBM has yet to fully leverage its large installed base and channel network.

- Mind share and go-to-market strategy: Market awareness of IBM’s EiPaaS solution remains low. IBM is still thought of as aligned predominantly with addressing the enterprise IT arena, rather than SMBs, lines of business and multipersona-oriented opportunities. This is partly due to IBM being generally viewed as a software company rather than a cloud company. IBM plans to broaden awareness of its EiPaaS efforts through a more unified go-to-market approach, including leveraging its significant internal and partner networks.

Informatica

Founded in 1993 and based in Redwood City, California, U.S., Informatica is a large, privately owned company and one of the most successful players in the data management market. The company’s EiPaaS solution is the Informatica Intelligent Cloud Services (IICS), part of the Informatica Intelligent Data Platform proposition. This also includes application integration, APIs, B2B, integration hub, data integration, data quality, data catalog, big data management, data security and MDM services, which are increasingly enabled by Informatica’s CLAIRE metadata-driven AI and ML engine.

IICS is available with a base package along with use-case-based packaging and pricing that cover a range of integration scenarios.

Strengths

- Customer experience: In 2017, Informatica added 1,500 new clients, reaching an installed base of more than 8,500, and grew revenue by more than 50%, to approximately $190 to $200 million, retaining its position as the largest iPaaS provider. Reference customers evaluated Informatica as one of the best vendors in this Magic Quadrant for overall customer experience, and above average in services, product value for money, and quality and flexibility of the sales process.

- Product functionality and developer experience: IICS provides a wealth of data, application, process, API-based and B2B integration, as well as data quality and security functionality — including Service Organization Control 2 (SOC 2), SOC 3 and HIPAA support. Reference customers scored the platform as above average for core integration features, integration specialist and ad hoc integrator experience, and reliability.

- Innovation: Informatica was one of the first EiPaaS providers to leverage, via CLAIRE, AI and ML technologies to improve the user experience and optimize operations. In 2017, the company re-engineered the platform based on an advanced microservices and metadata-driven architecture, which enables a unified user experience and improved quality of service for clients.

- Sales and geographic strategies: Informatica plans to double its cloud sales specialist organization and to strengthen its midmarket-focused inside-sales team. The planned availability of the platform on AWS, Microsoft Azure and other second-tier clouds will make it increasingly appealing for organizations engaging in multinational and global initiatives.

Cautions

- API management: Despite the planned introduction of an API developer portal and improvements in the API gateway functionality, the IICS API management capabilities are still behind those of several competitors in maturity and functionality. Reference customers scored Informatica’s policy management capability as being below average.

- Client perception: Although the company is one of the top three EiPaaS providers in terms of visibility in the market, prospects perceive IICS as being primarily focused on data integration and therefore rarely consider it for API-centric use cases.

- Offer complexity: IICS has reached a level of sophistication that may be overwhelming. Although Informatica is rolling out modular use-case-based packages, should its sales and marketing organizations fail to articulate such a complex value proposition in simple terms, the less technically savvy prospects will struggle to understand and appreciate the offering.

- Citizen integrators: Although Informatica recognizes the citizen integrator role and plans for chatbot support, the IICS roadmap does not address the use of natural-language recognition to empower this audience, which other providers have or plan to have.

Jitterbit

Established in 2003, Jitterbit is a private company based in Alameda, California, U.S. Jitterbit originated as a provider of integration software focused on the SMB market. In 2010, Jitterbit began providing Jitterbit Enterprise Cloud Edition, an EiPaaS rendition of its on-premises product.

Jitterbit’s Harmony platform, which was released in 2014 as an evolution of Enterprise Cloud Edition, provides support for the integration of diverse cloud, interenterprise and on-premises environments, as well as API autocreation and API management. Jitterbit also provides solutions for ISVs and SaaS providers, including prebuilt templates for various common cloud and on-premises integrations in order to deliver embedded integration capabilities. Jitterbit offers a free 30-day trial of its EiPaaS solution.

Strengths

- Market responsiveness: With monthly major releases and weekly minor releases, Jitterbit is in a position to respond rapidly to market demand, as shown by the addition of native API management capabilities and Salesforce Platform Events during 2017.

- Platform versatility: As well as the standard application and data integration use cases, Jitterbit clients reported using the platform for API management, B2B/EDI and IoT use cases — highlighting the versatility of the platform.

- Customer experience: Jitterbit received one of the highest scores for customer satisfaction from its reference customers, at both a product and a vendor level, and received an unconditional recommendation from its reference customers. This was achieved while growing revenue above the market average and adding more than 400 new client organizations and 10,000 new freemium users.

- Broad platform vision: The Jitterbit Harmony platform is becoming more appealing for strategic adoption. This is due to a combination of good provision for the different integration personas, including the digital integrator, plus improved collaboration tooling and a strong roadmap with more AI and serverless runtime options.

Cautions

- Geographic presence: The 12% of Jitterbit’s client base in Asia/Pacific has to use global data centers in Europe and North America to create and manage its integrations. Jitterbit does provide a regional data center in Australia for the runtime component, as well as clients being able to download and deploy the runtime themselves. There are plans to open a dedicated Asia/Pacific data center in 2018, including the management component.

- Market positioning: Jitterbit’s go-to-market strategy has historically targeted the SMB segment, with the result that some larger enterprises do not consider Jitterbit in their initial selection process. This positioning from Jitterbit changed during 2017, but it might take some time for market perceptions to change.

- Rapidly evolving platform: During 2017, many new features were added to the Harmony platform, including major components such as API management, Salesforce Platform Events and new collaboration features between the various developer personas. Some clients have reported they wish to see improved documentation and guidance on these new features, or that some aspects of the platform are less mature than those offered by the competition.

Microsoft

Founded in 1975 and based in Redmond, Washington, U.S., Microsoft made Azure Logic Apps generally available in July 2016, as a stand-alone EiPaaS offering. From 2018, Azure Integration Services will be the collective name for a number of integration-related components, including Logic Apps, API Management, Service Bus and Event Grid. Data Factory rounds off the EiPaaS offerings for extraction, transformation and loading (ETL)-type workloads. Microsoft Flow, built on top of Logic Apps, enables citizen integrators.

Strengths

- Global cloud: Deployed in more than 30 of Microsoft’s cloud regions globally, with another six planned for 2018, Azure Integration Services are widely available in most regions. The addition of Azure Stack, Microsoft’s Azure on-premises extension, increases runtime deployment options and support for hybrid scenarios, and removes the historic dependency on BizTalk.

- Strong growth: Gartner estimates that Microsoft more than tripled its client base during 2017, making it one of only a handful of vendors with more than 5,000 client organizations. Microsoft’s was also the fourth most considered platform among those offered by the vendors in this Magic Quadrant, reflecting its increasing market presence.

- Platform versatility: During 2017, Microsoft added numerous features to its EiPaaS offering to improve its versatility, which now covers application integration, data integration, API management, B2B/EDI and IoT scenarios. This versatility of use was also confirmed by Microsoft’s reference customers.

Cautions

- Platform maturity: Microsoft has responded to feedback around a lack of functional depth in the offering by having an aggressive release schedule during 2017. While this has been recognized as a strength, many of these capabilities are still relatively unproven in the market. This is reflected in its reference customers’ evaluations, with many of the features receiving below-average scores, including protocol mapping, data formats, data standards and data mapping and transformation.

- Microsoft-developer-focused ecosystem: With such a large customer base to leverage and a strong focus on the enablement of developers, Microsoft often fails to market to the buyers of SaaS, including Microsoft SaaS. This results in a message that does little to appeal to organizations that do not have Microsoft development skills, though Flow goes some way to addressing this.

- Customer expectation: While reference customers’ satisfaction was generally good, the EiPaaS market is an incredibly competitive space with the majority of vendors being scored above 4.5 on a 1 to 5 scale in both product and vendor satisfaction. Microsoft scored just below average on overall satisfaction and just above average on value for money, and has some work to do in this area if it wants to catch up with the leading competition.

Moskitos

Incorporated in 2012, and based in Levallois-Perret, France, Moskitos is a cloud service provider entirely focused on EiPaaS. The company, funded by private investors and French government grants, operates primarily in France, Belgium, Switzerland and the U.K., and has plans for an office in Asia/Pacific in 2H18.

Moskitos’ EiPaaS solution, Crosscut, was launched in 2013 and provides a range of data, application and IoT integration functionality and API management. Crosscut is implemented on Microsoft Azure, but the company is working on a containerized version of the platform to support multicloud scenarios.

Strengths

- Customer satisfaction: Reference customers scored Moskitos as second-best for value for money, and well above average in overall customer satisfaction, core platform functionality, user experience and professional services.

- Sales execution: Despite its small size, in 2017 Moskitos doubled its installed base to almost 5,000 paid direct and, mostly, indirect clients. Such growth was achieved by increasing visibility in its countries of operation (especially France) and by orchestrating partnerships with local SaaS players: SIs, such as Accenture, DXC Technology and Akatoa; and technology partners such as Axway, CA Technologies and OpenDataSoft.

- Offering versatility: Through a combination of internal developments and technology partnerships, Moskitos has developed Crosscut into a versatile EiPaaS solution. Clients are using Crosscut for integration of cloud and on-premises applications, data, B2B and mobile apps as well as for API management. Moreover, Moskitos has invested significantly to improve the Crosscut user experience, community support and operations. The company also plans to add MFT and ETL capabilities, thus increasing Crosscut’s appeal for organizations looking for a versatile and functionally rich EiPaaS solution.

Cautions

- Operations: Moskitos is a small, 30-employee company mostly focused on France and neighboring countries. It has a network of about 20 SI partners and outsources its 24/7 support operations to a third party (Codit). The company also plans to support Crosscut on multiple cloud infrastructures (such as AWS, Microsoft Azure and Alibaba Cloud). However, it may still have a limited appeal for organizations that require local commercial presence and support in their country.

- Viability: Despite significant high-double-digit growth, Moskitos’ large customer base generates quite modest revenue because the majority of sales are indirect, SMB clients (pharmacies and car dealers). This level of revenue is unlikely to generate the resources needed to sustain the company’s ambitions in the long term, which would require substantially increased external investment.

- Sales and marketing strategy: Moskitos’ marketing has progressed during the past 12 months, and the company plans new initiatives to target industry verticals and use cases through partners. The company plans to raise funding to expand in Asia/Pacific (Singapore) and also to set up a sales team to target OEM customers. Nonetheless, due to the limited financial resources available, Moskitos’ industry recognition and market share are likely to remain significantly lower than those of most of its competitors.

MuleSoft

Founded in 2006, and based in San Francisco, California, U.S., MuleSoft started as a provider of enterprise service bus (ESB) software and was one of the early vendors in the EiPaaS market.

In 2013, MuleSoft released Anypoint Platform, a combination of EiPaaS, API management and ESB technology. Since then, MuleSoft has added Anypoint Exchange, a collaboration and sharing tool; Anypoint MQ, a cloud messaging capability; and Anypoint Design Center’s flow designer, a cloud-based integration developer experience targeting ad hoc integrators.

On 20 March 2018, Salesforce entered into a definitive agreement to acquire MuleSoft. This acquisition was not closed at the time of our research for this Magic Quadrant, or its publication, so the evaluation of MuleSoft is based solely on its capabilities as a stand-alone company.

Strengths

- Brand awareness: MuleSoft enjoys broad, global market awareness based on its open-core ESB, strong API management capabilities and EiPaaS offering. For three years in a row, it was the vendor most often considered by the reference customers for Gartner’s EiPaaS survey, and is one of the top three vendors discussed on integration inquiries with Gartner during 2017.

- Strong revenue growth: Gartner estimates that MuleSoft’s revenue grew above the market average in 2017, which makes it one of a handful of vendors generating around $100 million or more from EiPaaS revenue. With strong and increasing renewals and a focus on larger strategic clients, MuleSoft has established itself as a player in the broader integration market.

- Platform availability: MuleSoft’s Anypoint Platform is deployed across 12 data centers around the world and leverages the latest in platform availability at both a local and regional level. MuleSoft plans additional capabilities to ease multicloud deployments during 2018. The Anypoint Platform is one of the most highly available EiPaaS offerings around.

- Platform versatility: MuleSoft’s Anypoint Platform has features targeting application integration, data integration, API management, B2B/EDI and IoT initiatives, as well as a strong product roadmap that includes AI/ML for improved integration delivery.

Cautions

- Customer experience: MuleSoft’s reference customer satisfaction ratings declined from last year in both vendor and product satisfaction. Gartner feels that this can be partly explained by the company’s go-to-market strategy of focusing on larger, more strategic opportunities, which, by their nature, will be more complex to implement.

- Client base growth: MuleSoft reported adding just over 100 enterprise organizations during 2017, which is well below the market average. However, the number of users of the platform grew above the market average, reflecting an increase in use by current clients as well as by new clients with a large user base.

- Strong focus on integration specialists: Given the history of MuleSoft in application integration, it is common knowledge that clients get the most out of MuleSoft if they have good technical skills. While MuleSoft has started to address the ad hoc integration persona, with the release of Flow designer, it still has some work to do regarding ease of use for nontechnical users. This is reflected in its low customer reference scores for ad hoc and citizen integrator user experiences.

- Marketing strategy: MuleSoft’s Anypoint Platform is marketed as a unified platform for API-led connectivity. It is available in both software and as-a-service delivery models, and a hybrid mix of the two. While this is appropriate for some large-scale strategic deployments, some Gartner clients have reported that they found this confusing when looking for an EiPaaS solution.

Oracle

Founded in 1977 and based in Redwood Shores, California, U.S., Oracle offers a spectrum of EiPaaS technologies that have co-evolved alongside the underlying infrastructure that Oracle provides through IaaS, PaaS, SaaS and application and data integration technologies. Oracle has leveraged this set of capabilities to provide the Oracle Integration Cloud.

The Oracle Integration Cloud Service (ICS) primarily addresses the high-productivity EiPaaS requirements of ad hoc integrators. Oracle’s service-oriented architecture (SOA) Cloud Service, a PaaS rendition of part of the on-premises Oracle SOA Suite, is a high-control platform targeting specialist integrators. Oracle has various other xPaaS offerings that can be combined with its EiPaaS. These xPaaS offerings include: Oracle Process Cloud Service, for improved orchestration and business activity monitoring; Oracle Data Integration Platform Cloud, to support data manipulation and sharing. Also, Oracle Apiary and API Platform Cloud Service, for API management; Oracle Managed File Transfer Cloud Service, for managed file transfer; and Oracle IoT Cloud Service, for IoT integration.

Strengths

- Resonance with PaaS market demands: Oracle’s EiPaaS development and roadmap address the diverse capabilities and use cases in this market and capitalize on enabling HIP approaches. A go-to-market strategy drawing on a synergistic focus between its EiPaaS and other Oracle PaaS and SaaS technologies, brings together Oracle’s portfolio. An emphasis on supporting IoT integration, and a mix of application and data integration, data sharing and governance opportunities capitalizes on demand trends.

- Brand awareness and market presence: Oracle’s size and global coverage of applications and analytics solutions enable it to draw on a huge customer base and a wide product distribution model for positioning its EiPaaS offerings. Oracle rapidly expanded its EiPaaS installed base during 2017, to almost 3,000 customers — to nearly triple in size. Broad usage of Oracle’s technologies within its customer base has driven wide availability of community support, training and third-party implementation practices.

- Offering strategy capitalizes on evolving trends: EiPaaS functionality as part of a broad solution set positions Oracle well to compete with major competitors who have an established EiPaaS specialization in this market. Evolving an offering strategy around enabling autonomous cloud integration and ML-based recommendations for APIs, along with approaches for contextual and chat-based search interfaces, extends integration delivery for digital business transformation.

Cautions

- Integrated usage and support across portfolio: To facilitate a seamless expansion of deployments across use cases, reference customers expressed their desire for improvement in technical help and simpler integrated use of EiPaaS tooling with Oracle’s other products.

- Complex offering model: Concerns about Oracle’s customer engagements were reported by its reference customers. These involved challenges with navigating pricing models and the billing arrangements, and determining appropriate licensing across the extensive range of EiPaaS solutions and deployment choices. Oracle’s recently introduced Universal Cloud Credit model sets out to simplify how customers order and procure Oracle’s cloud-related offerings.

- Implementation delivery: Implementation delivery, a longer learning curve and technical guidance including documentation, are cited as challenges by Oracle’s reference customers in some circumstances when implementation requirements and complexity grow. Customers desire easier ways to accomplish platform administration and team-based development.

SAP

Founded in 1972 and based in Walldorf, Germany, SAP’s EiPaaS offering is framed in its broader PaaS strategy called SAP Cloud Platform (CP). With its integration-related capabilities, SAP CP supports multiple use cases and includes functionality for application, data, process and B2B integration; stream analytics; workflow; API management; IoT integration; batch and real-time data replication/synchronization; and data quality. SAP CP is available in non-SAP cloud infrastructure including AWS, Google Cloud Platform and Microsoft Azure.

Those capabilities leverage the SAP HANA in-memory DBMS and are available in different packages, including SAP Cloud Platform Integration (CPI), SAP Cloud Platform API Management and SAP Cloud Platform for the Internet of Things.

Strengths

- Broadening usage and extensive functionality: SAP’s EiPaaS technologies are used for diverse use cases and deployed in conjunction with SAP’s broad portfolio, with a vision for simplifying integration powered by its in-memory computing infrastructure. A focus on IoT-, API- and AI-enablement, alongside other SAP offering strategies in multicloud and data hub, enhances relevance for applications, data and analytics scenarios, to utilize rule-based autoscaling, self-healing and an ML-enabled integration solution advisor.

- Portfolio ecosystem: Customers value the linkage of SAP’s EiPaaS and adjacent products — for application and data integration, self-service data preparation, information governance and master data management — in combination, for solving complex problems in the SAP landscape. CPI provides an expanding range of prepackaged integration flows for SAP’s SaaS applications, including SuccessFactors, Ariba, Concur and S/4HANA Cloud.

- Market presence and growth: With approximately 1,500 new EiPaaS customers added during 2017, SAP’s pedigree as a large incumbent provider of applications and analytics solutions positions it to capture significant EiPaaS revenue and growth by leveraging its broader customer base.

Cautions

- Integration of product components: SAP continues to simplify seamless use between EiPaaS and its broader portfolio. However, making multiple tools work together across EiPaaS and the diverse integration offerings of SAP, is reported by its reference customers as a challenge — an area that SAP continues to focus on in maturing its offerings.

- Customer experience: SAP’s reference customers’ feedback indicates below-average satisfaction with quality, consistency and response in the processes for assisting with implementation and issue resolution. This adversely affects customer experience and the perception of value relative to cost.

- Product messaging: Some prospects and buyers, particularly organizations with an awareness of the individual products that existed before the integration packaging as part of SAP Cloud Platform, indicate a need for improved clarity and guidance during EiPaaS evaluations. SAP’s efforts to address these needs include a recently published CIO Guide for Integration, professional services to assist with adoption of CPI integration flows, and associated readiness-check and guidance for best practices.

Scribe Software

Founded in 1995 and based in Manchester, New Hampshire, U.S., Scribe Software is a provider of integration technology platforms.

The Scribe Online platform is a multitenant EiPaaS offering with a number of different licensing models. Integration Service is the general-purpose EiPaaS subscription. Replication Service is a data synchronization subscription to enable users to get data from their application portfolio into an analytics tool. Migration Service is a short-term service providing data migration capabilities between existing applications and their replacements. The platform/OEM/distributor model enables SaaS providers to include Scribe as part of their offering.

Strengths

- Integration developer productivity: Scribe Online’s most recent UI (released in 4Q16) provides ad hoc integrators with a straightforward method of developing, testing and managing integration flows. Scribe released a new developer success portal in 2017. This portal provides access to self-guided learning aids, a developer forum and tools (such as its full platform API, and two methods for building customer connectors — a fast framework for proofs of concept and a full connector development kit).

- Go-to-market strategy: Scribe has had historical strength through its partner channel and its focus on the midmarket segment. Scribe’s “partner first” design includes capabilities that ease end-user management (particularly for managed service providers), and a full API to their entire platform. However, direct (to end user) and enterprise sales have become an increasing focus. The year 2017 saw the added ability to purchase Scribe’s integration services through Salesforce AppExchange and Microsoft AppSource. Scribe Online’s 1,200 SIs are a testament to its desire to work with partners, but also a benefit for direct customers looking for outsourced integration help.

- Customer experience: Scribe’s customer reference scores put it among the top 30% in this Magic Quadrant in terms of overall satisfaction with the product, vendor and value.

Cautions

- Platform versatility and innovation: While Scribe Online is good for typical cloud service integration scenarios, it lacks capabilities that would enable it to be the fully featured tool which enterprise EiPaaS customers look for. For example, there is no native support for EDI-style B2B integration. Also, while the platform can publish APIs in the Open Services Access (OSA)/Swagger standard and connect to other enterprise API management products, the platform provides no native API management capability. While there are some starter packs for common integration flows among the endpoints, there is no application of ML techniques for suggesting next steps — unlike the solutions of the leading EiPaaS vendors.

- Market presence: Scribe has expanded its geographic presence by deploying a control plane to EMEA, and plans to expand into Australia during 2018. While it has recently invested in its commercial operations in order to support larger enterprises, it has historically been less visible in competitive evaluations of the EiPaaS market, particularly those outside North America.

SnapLogic

Founded in 2006, and based in San Mateo, California, U.S., SnapLogic offers Enterprise Integration Cloud for data and application integration, which is used by more than 1,275 enterprise customers. SnapLogic offers a rich set of native iPaaS capabilities to support cloud and on-premises applications, APIs, analytics, big data and IoT integration use cases.

SnapLogic provides an intuitive web-based user interface for specialist, ad hoc integrators and citizen integrators. Users can leverage the vendor’s more than 450 adapters (Snaps), develop pipelines (integration flows that can be turned into REST APIs that return data when invoked), and create/find/modify reusable patterns.

Strengths

- Client growth and market traction: SnapLogic added 525 customers in 2017, which represented a 70% increase over 2016 and was well above the market average. It also extended its partner network to more than 60 partners, introduced a midmarket strategy and pricing, expanded its free trial offering, and appointed new senior sales and partnership leaders.

- Product innovation and evolution: SnapLogic supports hybrid deployments and a variety of use cases, particularly for analytics and big data integration, along with SaaS integration and basic API integration. In 2017, SnapLogic launched Iris AI, its AI and ML-based capabilities to help improve integration accuracy and to speed up routine integrations. As an early mover in leveraging AI in EiPaaS, SnapLogic has demonstrated product innovation and has a roadmap that includes enhancing AI-based capabilities and use cases.

- Customer experience and extensive deployment: Reference customers scored SnapLogic as above average in overall customer satisfaction and experience, value for money and delivery and execution. This performance helped SnapLogic drive the highest, and significantly above average, number of projects and implemented integration flows and processes per customer in this Magic Quadrant.

Cautions

- B2B, API managementand ecosystem community features: SnapLogic does not offer its own B2B integration to support EDI interactions, or provide full life cycle API management capabilities. For full life cycle API management, SnapLogic partners with Apigee and 3Scale (both of which have been acquired in recent years), and Orderful for B2B integration to support EDI. SnapLogic relies on these partners to provide ecosystem community features such as API developer portals and B2B partner portals; however, reference customers scored SnapLogic as below average for these features. To help address some of these gaps, SnapLogic’s roadmap includes increasing investment into both its core product and its partnerships; for example, involving Apigee, and API tooling through Swagger.

- Market awareness and positioning: Although SnapLogic increased its revenue share from regions outside of North America in 2017, it is still less visible than some EiPaaS competitors outside of this region. It is often not viewed by large companies as a strategic middleware partner. This suggests that SnapLogic has yet to see the full benefits of its increased investment in marketing, partnerships and geographical expansion in EMEA, Latin America and Asia/Pacific.

- Developer user interface and experience: Some SnapLogic reference customers raised issues relating to its development user interface. These included having higher expectations of the overall UI experience for more technical users — in the form of better navigation and more online documentation, for example. Such implementation-related challenges could affect SnapLogic’s otherwise solid customer experience scores.

Workato

Workato, based in Cupertino, California, U.S., is a private company fully dedicated to the EiPaaS market. Founded in 2013, Workato first released its EiPaaS offering in the same year. Investors include Storm Ventures, Salesforce and Workday.

The Workato EiPaaS solution is available in five editions (Base, Professional, Business, Business Plus and Enterprise Platform) differentiated by functionality, amount of consumable resources (connections, transactions, job history store, polling intervals) and level of support. These editions are also available at a discounted price for not-for-profit organizations. All the editions are freely available for a 30-day trial and a Community Edition is available free of charge for individual citizen integrators.

Strengths

- Customer experience: Workato got the top scores from its reference customers in all the customer experience-related criteria, including overall experience with the provider, delivery and execution, sales process, contract flexibility, SLAs, services and value for money.

- Product: The functionally rich, versatile and enterprise-class Workato EiPaaS solution appeals to a full range of buyers thanks to its powerful development tools, ML-enabled user experience, and governance tools accessible also to nonprofessionals via a bot platform (Workbot). Reference customers rated all its functionality as above average, often significantly so.

- Innovation: Workato was one of the first EiPaaS providers to deliver a rich set of AI-enabled capabilities to assist integration developers. In 2018, the company plans to extend its use of AI in areas such as security, optimization and self-healing, robotic process automation support, connectors’ configuration and autogeneration of simple integration flows.

- Sales strategy: In addition to its own direct sales organization, Workato relies on partnership with key SaaS providers (Salesforce, Workday and Slack), regional SIs, and on OEM sales. It initially targets citizen and ad hoc integrators, but ultimately aims at enterprise IT. In this way, it has collected about 3,500 clients during the past five years, tripled revenue in 2017 — which was well above the market average — and plans for further substantial growth in 2018.

Cautions

- Geographic strategy: Workato generated 46% of its 2017 revenue from outside North America, primarily through partners, and has a good direct presence in Asia/Pacific. However, in EMEA it only has a small staff, which is probably insufficient to support a large number of enterprise clients in the region.

- Versatility: Workato does not yet provide EDI B2B integration capabilities. Moreover, Workato’s lack of an on-premises deployment option for the platform’s runtime executive makes it of limited interest for organizations with demanding, low-latency, ground-to-ground integration needs or severe security constraints and compliance.

- Operations: Despite support from several regional SIs, and with a team of about 90 employees mostly based in the U.S. and India, the company may not be attractive to user organizations requiring local commercial presence and support in their country.

- Mind share: Only a handful of reference customers mentioned Workato as an offering that they had considered, and discarded in favor of other providers. This indicates a still scarce awareness in the market, at least outside of North America and especially among enterprise IT buyers.

Vendors Added and Dropped

We review and adjust our inclusion criteria for Magic Quadrants as markets change. As a result of these adjustments, the mix of vendors in any Magic Quadrant may change over time. A vendor’s appearance in a Magic Quadrant one year and not the next does not necessarily indicate that we have changed our opinion of that vendor. It may be a reflection of a change in the market and, therefore, changed evaluation criteria, or of a change of focus by that vendor.

Added

Dropped

- Actian

- Attunity

- Fujitsu

- Terrasky

- Youredi

Inclusion and Exclusion Criteria

The inclusion criteria represent the specific attributes that analysts believe are necessary for inclusion in this research.

To qualify for inclusion, vendors must deliver a service with the following characteristics.

- It has to be a cloud service:

- Available by subscription and accessible over internet technologies

- Available uniformly to all qualified subscribers

- Including some sharing of physical resources between logically isolated tenants (subscribers or applications)

- Including some self-service provisioning and management by subscribers

- Including bidirectional scaling without interruption of activities and with some automation

- Including some instrumentation for resource use tracking

- It has to be a PaaS solution:

- It encapsulates the underlying virtual or physical machines, their procurement, management and direct costs, and does not require tenants to be aware of them.

- It delegates to the providers the patching, versioning and health of the platform stack.

- It has to provide the following iPaaS capabilities:

- Features targeting application integration (that is, the ability for different applications to exchange messages, call each other’s business functions, automate business process)

- Features targeting data integration (that is, the ability for different data stores to synchronize, to move data from one to the other, to combine and aggregate data from different stores)

- Connectivity to different endpoints for on-premises and cloud, including:

- Application connectors (for example, Salesforce, Oracle E-Business Suite, SAP S/4HANA and others)

- Data source connectors (for example, file systems, SQL and no SQL databases)

- Technology connectors (for example, FTP, HTTP, Java Message Service (JMS), Open Database Connectivity (ODBC) and others)

- Multiple data/message delivery styles including:

- API-based

- Messaging-based

- Batch

- Data and message validation

- Data and message mapping and transformation

- Data and message routing and orchestration

- End-user tools to develop, test, deploy, execute, administer, monitor and manage integration flows and to manage the life cycle of the relevant artifacts (transformation maps, routing rules, orchestration flows, adapter configurations and others)

- It has to be enterprise-grade and aimed at enterprise-class projects, by providing:

- Support for HA/DR

- Secure access to endpoints and to the platform functionality

- Technical support to paying subscribers

- It has to be marketed for a broad range of use cases, verticals and industries.

- It has to be provided as a “stand alone” service directly usable by the subscriber. To use the platform, clients can subscribe to the EiPaaS capability only, not just to some other cloud service — a SaaS application or another form of PaaS, such as aPaaS, of which the iPaaS capabilities are an “embedded” subset.

- It has to be generally available as of 1 November 2017, with at least 600 paying client organizations by the same date. Please note that we take into account the number of paying organizations and not individual users. We consider both “direct” and “indirect” clients (that is, organizations that bought a provider’s EiPaaS solution via a reseller or OEM partner).

Evaluation Criteria

Ability to Execute

Ability to Execute criteria aim at evaluating a provider’s ability to deliver an EiPaaS solution that offers the expected set of functions, ensuring that customers’ integration projects succeed while growing providers’ revenue and market share. In this maturing market, where aggressive new entrants try to win new clients as fast as possible, the most important factors for success are:

- The platform’s ability to provide a broad set of capabilities targeting a wide range of client use cases (Product or Service criterion).

- The provider’s proven track record of enabling integration projects to succeed through responsive support, adequate pricing and the ability to establish positive commercial relationships (Customer Experience criterion).

Other important elements for success in the enterprise iPaaS market are:

- The provider’s installed base and ability to build up a credible and long-term business (Overall Viability criterion).

- The provider’s ability to deliver on the sales strategy with competitive, flexible pricing models for different targeted buyers (Sales Execution/Pricing criterion).

- A proven track record in keeping pace with evolving market requirements (Market Responsiveness/Record criterion).

- The provider’s effectiveness in generating brand awareness and stimulating prospect interest through sound marketing campaigns (Marketing Execution criterion).

- A strong global sales and marketing structure and support/professional services, a vast partner network and multiple, geographically distributed data centers (Operations criterion).

Product/Service: Core goods and services offered by the vendor for the defined market. This includes current product/service capabilities, quality, feature sets, skills and so on, whether offered natively or through OEM agreements/partnerships. As defined in the Market Definition section and detailed in the following subcriteria: enterprise worthiness, openness, integration developer productivity, ease of operations, citizen integrator support, platform versatility, core integration features, ecosystem/community support features, policy management and enforcement.

Overall Viability: Viability includes an assessment of the overall organization’s financial health, the financial and practical success of the business unit. Also, the likelihood that the individual business unit will continue investing in the product, will continue offering the product and will advance the state of the art within the organization’s portfolio of products. Important subcriteria are product revenue, profitability, and research and development investment ratios.

Sales Execution/Pricing: The vendor’s capabilities in all presales activities and the structure that supports them. This includes deal management, pricing and negotiation, presales support, and the overall effectiveness of the sales channel. Items of importance here are transparency in pricing, ease of access for evaluation and client growth rates.

Market Responsiveness/Record: Ability to respond, change direction, be flexible and achieve competitive success as opportunities develop, competitors act, customer needs evolve and market dynamics change. This criterion also considers the vendor’s history of responsiveness. The subcriteria followed here were frequency of release schedule, adjustment of platform features based on client demand, and anticipation of market direction.

Marketing Execution: The clarity, quality, creativity and efficacy of programs designed to deliver the organization’s message. This message is designed to influence the market, promote the brand and business, increase awareness of the products and establish a positive identification with the product/brand and organization in the minds of buyers. This “mind share” can be driven by a combination of publicity, promotional initiatives, thought leadership, word of mouth and sales activities. Of specific interest, was the differentiation of buyer journeys, market presence and client perception.

Customer Experience: Relationships, products and services/programs that enable clients to be successful with the products evaluated. Specifically, this includes the ways customers receive technical support or account support. This can also include ancillary tools, customer support programs (and the quality thereof), availability of user groups, SLAs, and so on. Here, we paid particular attention to customer satisfaction with products, customer satisfaction with the vendor and willingness to recommend the offering to others.

Operations: The ability of the organization to meet its goals and commitments. Factors include the quality of the organizational structure, including skills, experiences, programs, systems and other vehicles that enable the organization to operate effectively and efficiently on an ongoing basis.

Table 1: Ability to Execute Evaluation Criteria

Enlarge Table

Evaluation Criteria | Weighting |

Product or Service | High |

Overall Viability | Medium |

Sales Execution/Pricing | Medium |

Market Responsiveness/Record | Medium |

Marketing Execution | Medium |

Customer Experience | High |

Operations | Medium |

Source: Gartner (April 2018)

Completeness of Vision

Completeness of Vision criteria aim to assess providers’ ability to meet the emerging requirements and drive enterprise iPaaS adoption (in new territories and toward a more strategic positioning), while also growing a profitable and self-sustaining business.

During the next 12 months, success in this market will, therefore, primarily depend on:

- Articulating differentiating value propositions and positioning in the market (Marketing Strategy criterion)

- Devising an effective and efficient sales strategy (Sales Strategy criterion)

- Having a roadmap capable of addressing new functional and nonfunctional requirements (Offering [Product] Strategy criterion)

- Formulating a geographic expansion strategy ( Geographic Strategy criterion)

Other important factors will include:

- The provider’s ability to understand the evolution of the iPaaS market (Market Understanding criterion), for example:

- Emerging use cases such as API management, MAI, big data and IoT integration

- The user organization’s growing focus on citizen integrators and adaptive/bimodal approaches to integration projects

- A general market trend toward the HIP approach to delivering integration capabilities

Market Understanding: Ability of the vendor to understand buyers’ wants and needs and to translate those into products and services. Vendors that show the highest degree of vision listen to and understand buyers’ wants and needs, and can shape or enhance those with their added vision. Key for the EiPaaS market is an understanding of the different integration personas and their buyer journey as well as the breadth of integration use cases.

Marketing Strategy: A clear, differentiated set of messages consistently communicated throughout the organization and externalized through the website, advertising, customer programs and positioning statements.

Sales Strategy: The strategy for selling products which uses the appropriate network of direct and indirect sales, marketing, service and communication affiliates that extend the scope and depth of market reach, skills, expertise, technologies, services and the customer base. Of special interest are the different approaches for direct sales, ISV/OEM sales and SI sales strategies.

Offering (Product) Strategy: The vendor’s approach to product development and delivery that emphasizes differentiation, functionality, methodology and feature sets as they map to current and future requirements. The subcriteria for this are enterprise worthiness, openness, integration developer productivity, ease of operations, citizen integrator support, platform versatility, core integration features, ecosystem/community support features, policy management and enforcement.

Business Model: The soundness and logic of the vendor’s underlying business proposition.

Vertical/Industry Strategy: The vendor’s strategy to direct resources, skills and offerings to meet the specific needs of individual market segments, including vertical markets. The subcriteria are platform ecosystems such as ERP, CRM and others; industry focus such as healthcare, education, retail and others; and vendor ecosystems such as Salesforce, Oracle, SAP and others.

Innovation: Direct, related, complementary and synergistic layouts of resources, expertise or capital for investment, consolidation, defensive or pre-emptive purposes. Specific focus is given to the application of AI and ML to ease integration challenges.

Geographic Strategy: The vendor’s strategy to direct resources, skills and offerings to meet the specific needs of geographies outside the “home” or native geography, either directly or through partners, channels and subsidiaries as appropriate for that geography and market. This includes, locations of the control plane deployment and the runtime plane deployment as well as the partner network.

Table 2: Completeness of Vision Evaluation Criteria

Enlarge Table

Evaluation Criteria | Weighting |

Market Understanding | Medium |

Marketing Strategy | High |

Sales Strategy | High |

Offering (Product) Strategy | High |

Business Model | Medium |

Vertical/Industry Strategy | Medium |

Innovation | Medium |

Geographic Strategy | High |

Source: Gartner (April 2018)

Quadrant Descriptions

Leaders

During 2017, the Leaders quadrant accounted for almost 30,000 clients and more than $600 million in revenue, representing more than half of the entire EiPaaS market. The vendors in this quadrant have client numbers in the thousands for their EiPaaS offering, and often many thousands of indirect users via embedded versions of the platform and through “freemium” options.

They have a solid reputation, with notable market presence and a proven track record in enabling multiple integration use cases — often supported by the large global networks of their partners. Their platforms are well-proven and functionally rich, with regular releases to rapidly address this fast-evolving market.

As the market evolves to provide further capabilities over the coming months and years, it is the Leaders that are best positioned to continue pushing their dominance, although leadership cannot be taken for granted. In the fast-moving EiPaaS market, one misstep could have catastrophic consequences.

Challengers

Challengers in EiPaaS have been in the market for several years and have notable installed bases of thousands of clients, with a mature offering that is proven for multiple integration scenarios. Challengers also have the financial strength and commitment to compete aggressively in the iPaaS market; consequently, they often offer a competitive platform, at least for certain verticals and use cases.

However, Challengers have a somewhat limited perspective on how the EiPaaS market will evolve, who the buyers are (and will be), what the use cases are and how user expectations will evolve. This results in their offerings being more narrowly focused than those of the Leaders. Typically, they pursue a more focused go-to-market strategy that follows their existing client base, creating a functionally more limited platform roadmap as a result. Their sales and marketing strategies are somewhat constrained by their more limited focus on the EiPaaS market.

Challengers have the potential to make the transition into leadership positions by articulating a more aggressive and ambitious vision and roadmap, and by putting extra sales and marketing focus on the EiPaaS space. However, they will have to carefully monitor the competition, because some of the best-executing Niche Players may turn into Challengers during the next 12 months.

Visionaries

Visionaries understand the specific requirements of this market and are innovating through a combination of technology, delivery models and go-to-market strategies. This year, it is interesting to note that all of the Visionaries see their EiPaaS offering as a key element of a broader integration strategy. This strategy combines software licensing, software subscriptions and as-a-service subscriptions, with EiPaaS being one of many channels for the underlying integration capabilities.

Visionaries’ Ability to Execute is lower than that of the Leaders, because of:

- A smaller installed base

- Unaggressive and reactive sales operations

- A lack of strategic commitment to the EiPaaS market, instead focusing on broader integration delivery choices

- Mixed results with regard to customer experience

All of the providers in the Visionaries quadrant have a background in traditional on-premises integration middleware; as such, they have a good understanding of enterprise integration challenges. However, they may not have the sales and marketing expertise required to sell outside of their traditional IT client base. They have entered the market through acquisition, by significantly re-engineering their on-premises products for the cloud or, in some cases, by developing a new iPaaS technology.

Some Visionaries are well-positioned to make the transition into the Leaders quadrant during the next 12 months, if they manage to execute on their vision, gear up their sales and marketing machines and improve the customer experience for their clients.

Niche Players

Niche Players are often small companies; in many cases, startups, most of which have entered the market during the past few years. They typically have a relatively narrow focus in terms of the use cases they support, the geographies they serve or the sales strategy they are implementing.