It’s always interesting

to hear what Wally Rhines – CEO of Mentor Graphics

(now a Siemens company) and a semiconductor/EDA veteran executive – has to say. Last week, at the Mentor Forum in Israel, Wally presented a well articulated speech trying to demystify what seems a major consolidation in the semiconductor field, as if this industry was maturing and “dying”.

In this post, I’d like to briefly describe my understanding as well as my misunderstandingson Wally’s views.

Let’s start by summarizing his take on the semiconductor market:

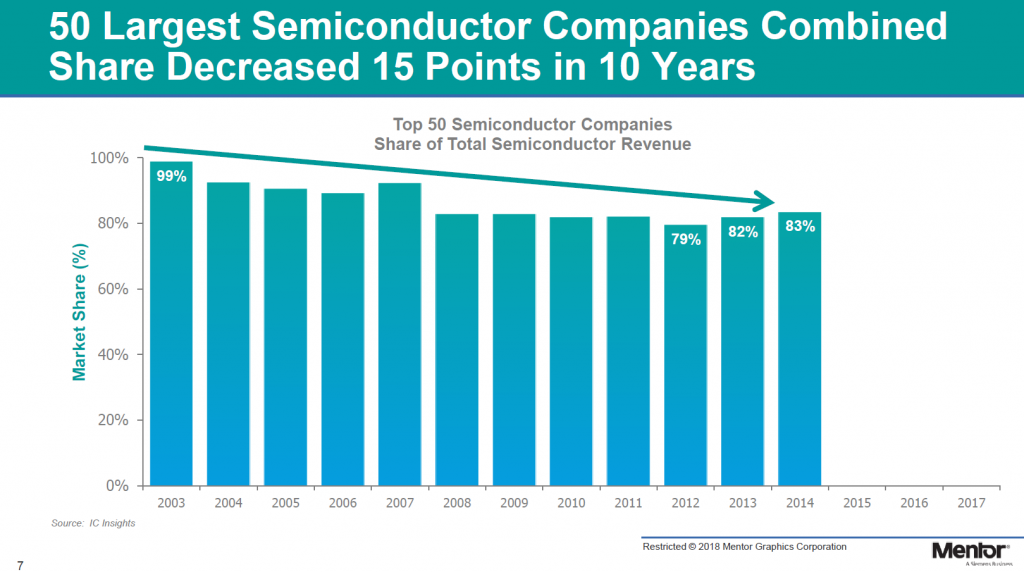

1) Wally showed that the market share of the 50 largest (or 10, 5, 1 largest) semi companies either decreased or stayed similar in the last many years.

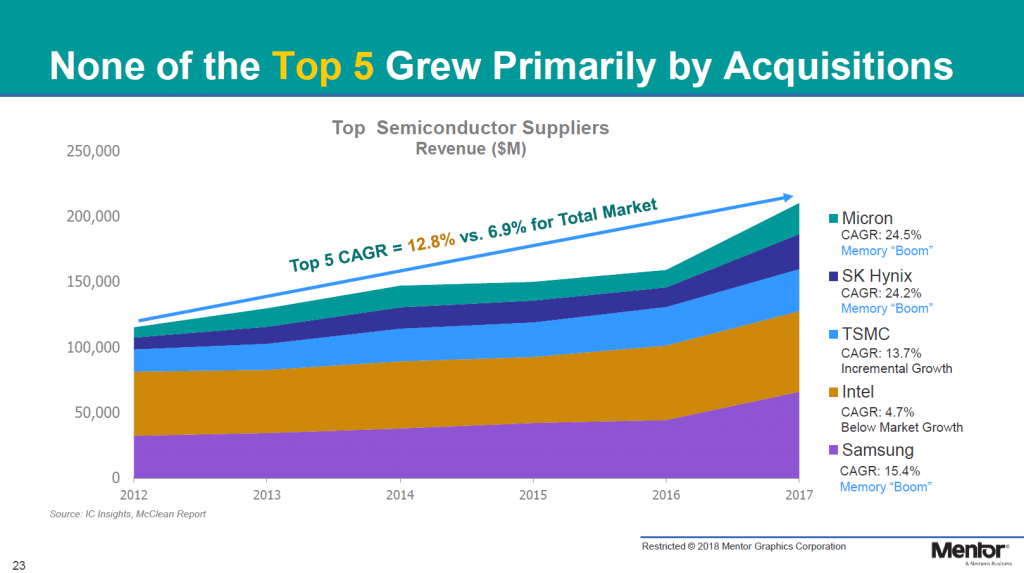

2) Most of the larger companies that expanded (such as Samsung and TSMC), did so by organic growth rather than through active M&A .

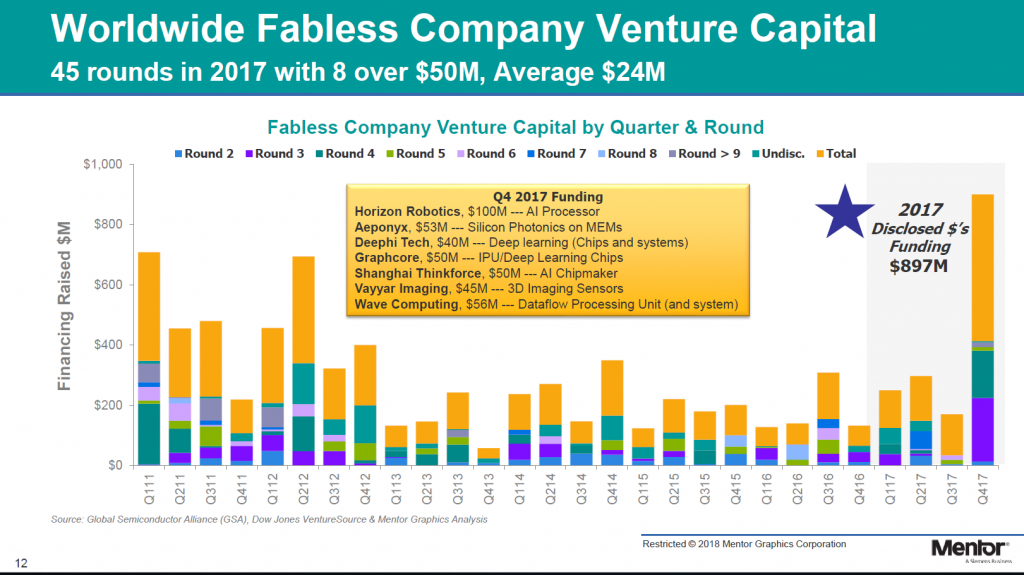

3) The extra market share is increasingly captured by start-up companies that are benefiting from unprecedented funding rounds.

4) Here we get to Wally’s key message: the companies benefiting the most from the active M&A trend, are those that are not just becoming bigger, but also more specialized.

For example, compare the following two types of companies:

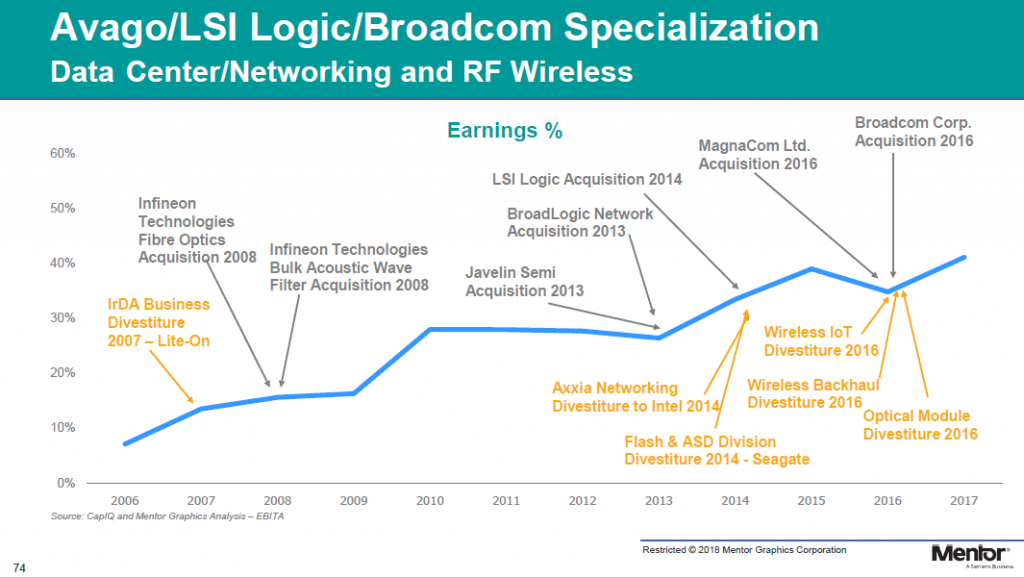

a) Today’s Broadcom, that also incorporated Avago and LSI Logic, is an example of specialization on data center/networking and RF wireless. Note the earnings moving from 10% a decade ago to ~40% today!

a) Today’s Broadcom, that also incorporated Avago and LSI Logic, is an example of specialization on data center/networking and RF wireless. Note the earnings moving from 10% a decade ago to ~40% today!

Other examples Wally brought in this category of specialization are Texas Instruments (Wally’s alma mater before joining Mentor) that specialized on Analog chips and NXP, focusing on automotive and security. But those 2 companies divested divisions almost as much, or more, than they acquired new companies.

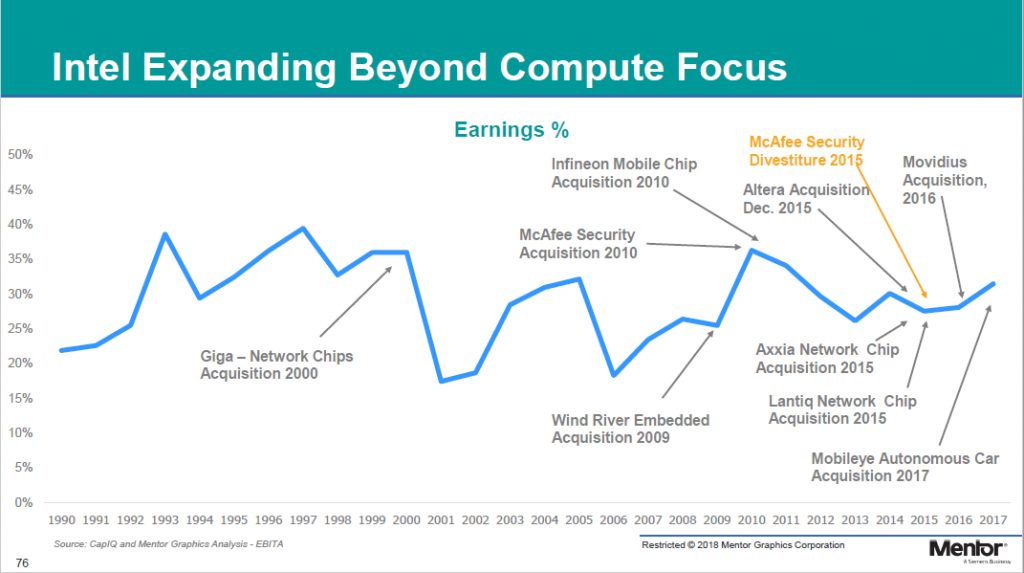

b) On the other hand, Intel has been buying all over the application spectrum, is moving to the other direction: from razor-sharp focus on CPU chips only to a very diversified portfolio. To Wally’s point, note their profitability’s ups & downs.

b) On the other hand, Intel has been buying all over the application spectrum, is moving to the other direction: from razor-sharp focus on CPU chips only to a very diversified portfolio. To Wally’s point, note their profitability’s ups & downs.

Wally’s bottom line: the semiconductor industry is alive and kicking! It’s not more consolidated than it was in the past (maybe even less!), it’s just growing & specializing and there is plenty of room (and $’s) for start-ups!

What about the EDA industry? Interestingly enough, it seems here we’re moving in the opposite direction.

a) Although I haven’t seen historical figures, it doesn’t seem to be undergoing any de-consolidation. The larger players – Synopsys, Cadence, Mentor (now a part of Siemens) and Ansys continue to capture the lion share of the market – 68% according to this report– with a very healthy appetite for acquisitions.

b) Neither I see any signs of specialization in EDA: Mentor itself is now part of Siemens’ large engineering software group, encompassing solutions for CAM, PLM, manufacturability besides traditional electronic design. Synopsys has long ago diversified to software and security solutions, besides its classic EDA tools and IP. Cadence is still primarily playing the same (specialized?) game, with some minor stretches into system design and verification.

True, the EDA market is a tiny ~10B$ pond compared ~400B$ semiconductors ocean – so the dynamics may be completely different.

Be it as it may, I believe that at least one aspect of the semi market will be closely followed by the EDA industry. Increasingly, major system and even software companies are designing their own customized chips – including Facebook, Google, Microsoft, Amazon and others. Therefore, the EDA expansion to system-level functions could just be a mirror-reaction to who their “new” customers are and what they do.